|

Not so natural monopolies |

To understand the logic underlying this measure, it is necessary to

go back a little, to the time when the telecommunications market was

first opened to competition.

The telecommunications sector, like transport and electricity

distribution networks, has the characteristic of relying on

infrastructure that is hugely costly to build and that, to be

profitable, must connect the greatest possible number of access

points. These costs, and the constraints of physical space, mean

that the dynamics of this sector do not correspond to the

traditional vision of competition. It is hard to imagine many

similar networks being superimposed to serve the same customers. The

first company to build an extensive network will always have a big

head start over the others.

For this reason, the conventional economic viewpoint has always

regarded telephone services as a “natural monopoly,” in other words

a sector whose very nature makes it impossible or highly improbable

that two producers will be competing with each other. Throughout the

world, telecommunications thus became a public utility controlled by

the state, so as to prevent any individual company the chance to

derive undue profit from the exploitation of this natural monopoly.

This way of seeing things has changed, however, and it is recognised

now that it is, in fact, possible for competitors to enter the field

by replicating at least part of the existing network and/or by using

different technologies to provide the same service. Thus, it is

possible nowadays to have a telephone conversation in various ways:

by sending an analogue or digital (IP) signal on traditional

wireline networks, by using software on a computer connected to the

Internet, by cable, by mobile telephone, and so on.

When the legal monopolies of incumbent operators in traditional

telephone services were abolished, regulators intervened with the

aim of offsetting the complete market domination these operators had

enjoyed for decades and creating a new balance between them and

their new competitors. In particular, they forced the former

monopolies to lease parts of their networks at advantageous rates to

the new entrants, enabling the latter to provide telephone and

Internet services without having to replicate the full

infrastructure throughout their territory. A company may thus

typically install its own fibre optic network between cities and

lease the local loop (the copper wires connecting the switch with

each home), thereby reaching customers directly.

|

Preventing discrimination |

Incumbent operators thus found themselves selling retail services to

individual customers and at the same time leasing wholesale services

(for instance, local loop access, an operation referred to in

industry jargon as “unbundling”(2))

to their competitors so that the latter can sell the same retail

services.(3)

One can easily imagine the conflicts of interest that may arise from

such a situation within a company. In order to maintain its market

domination, it could have an incentive to provide its competitors

with wholesale services of lesser quality than those it uses itself.

To prevent former monopolies from engaging in this type of

discrimination and using their dominant positions to prevent the

emergence of strong competitors, regulators have turned to various

solutions, including quality control of wholesale services,

accounting separation, and a prohibition on the sharing of certain

information between the units in charge of network management and

those selling retail services. In most countries where such measures

have been imposed judiciously, they have provided for the emergence

of alternative operators that are sufficiently dynamic to invest in

setting up their own networks and to compete directly with the

former monopolies.

Functional separation is a variation on this type of solution, but

it goes much further. It breaks up an operator’s vertical

integration and involves the creation of a fully separate division

in charge of network management to eliminate any ability or

incentive to discriminate against competitors. It is offered as a

radical type of intervention in cases where more moderate measures

would not have succeeded sufficiently in encouraging unbundling. But

is this remedy really necessary or effective?

The case of Britain, often used to show the pertinence of imposing a

reorganisation as drastic and costly as this, is far from

conclusive. In that country, local loop unbundling did not have much

success in the early years after the opening of access in 2001. In

2005, the market share held by BT (formerly British Telecom) in DSL

broadband lines—directly or through resellers—was still over 99%.

This failure led to measures that included the functional separation

of BT and the creation of an entity called Openreach to manage the

network.

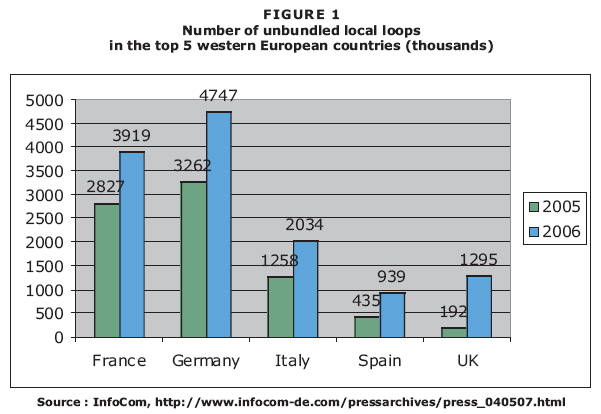

Since then, the number of local loops leased by alternative

operators has exploded (see Figure 1). But this phenomenon, far from

being limited to Britain, has affected all European countries. If

Britain has seen a high relative increase, it should be noted that

other countries have achieved higher levels of unbundling using

different methods. This is especially true of Germany and France,

which have not turned to functional separation.

|