|

There are those that consider the federal government’s new debt as “good debt.”

Minister Flaherty, for instance, likes to spin the $125 billion he will pay for

MBS as a revenue making opportunity for Canadians. The government’s interest

costs on government bonds, after all, are less than the interest it will

probably earn from its MBS investment, so it stands to make a profit on the

spread.

Don’t be beguiled by his talk. If the big banks need $125 billion in cash that

badly, why don’t they just sell their MBS in the open market? There is, after

all, an active secondary market for CMHC MBS in which sovereign wealth funds,

hedge funds, insurance companies, and pension funds participate.

The answer is that the banks prefer to sell their MBS to the government because

they’ll inevitably get better prices than if they were to sell on the market.

Try dumping $125 billion in assets on any market and smart buyers will smell

desperation and pull back, forcing that seller to drop prices. Having the

government step in and buy saves the bank from having to pay such a penalty. If

the government ends up paying $10 billion or so more than what the market would

have born, that means the big banks are being subsided to the tune of $300 per

Canadian. That’s a few hundred of their dollars that most Canadians will never

realize has gone to the banks.

It’s not the job of the state to add to its traditional role of public service

provider that of public hedge fund, nor should Flaherty start his morning

scanning a Bloomberg terminal for securities he can buy low and sell high with

taxpayer’s money. It’s the job of individual Canadians and their advisers to

decide on what makes a good speculation or market investment. Surely they won’t

be so eager to pay the banks above market prices like Flaherty has done.

Another reason some might call our new liabilities “good debt” is that the debt-funded

purchases of MBS takes illiquid securities off the books of Canada’s big banks,

providing them with cash which they might in turn lend out to credit-starved

Canadian businesses and consumers. “It’s for the greater good,” goes the

justification.

Consider the hidden costs of this move. Going forward, Canada’s banks now have

the incentive to add whatever sorts of illiquid debts they want to their balance

sheet. After all, a government that has already spent $125 billion buying

securities from bankers at above market prices will be able to twist the

taxpayer’s arm to do it again in the future. This only promotes irresponsibility

among bankers, weakens the Canadian banking system, and in the end serves as a

hidden tax on all Canadians.

What a shame to see our debt explode higher after years of steady cuts, and to

have these funds spent on investments that provide no verifiable net benefit,

and indeed impose hidden costs on individuals and the overall banking system.

Canada’s failed effort at reducing federal government spending only shows that

governments cannot be trusted to reduce their own size. In times of crisis, they

will inevitably seize the chance to grow ever larger again.

|

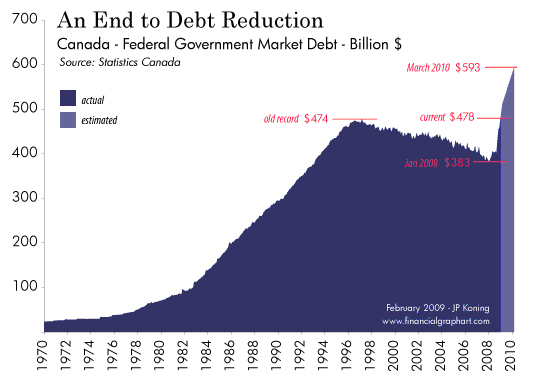

Subsequent Finance ministers John Manley, Ralph Goodale, and Jim Flaherty

chopped another $65 billion or so off the nation’s debts, and by early 2008 the

total would hit its lowest level in years: $383 billion, or around $11,600 per

Canadian. With the drop in debt came a corresponding drop in interest payments,

freeing up tens of billions of dollars for tax cuts and spending.

Subsequent Finance ministers John Manley, Ralph Goodale, and Jim Flaherty

chopped another $65 billion or so off the nation’s debts, and by early 2008 the

total would hit its lowest level in years: $383 billion, or around $11,600 per

Canadian. With the drop in debt came a corresponding drop in interest payments,

freeing up tens of billions of dollars for tax cuts and spending.