|

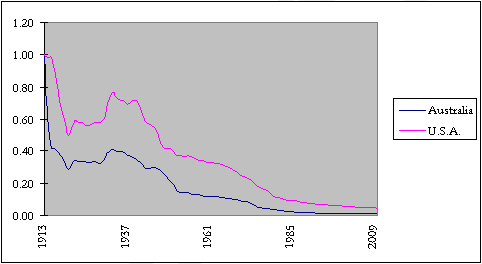

More specifically, Figure 2 shows

-

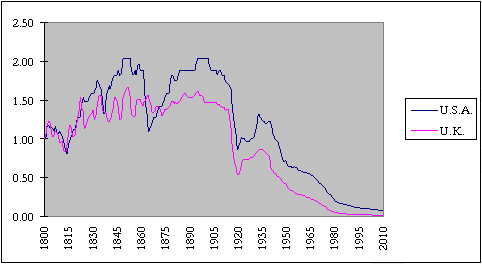

In 1800-1807, the PP of the dollar

rose by 16% (i.e., from $1.00 to $1.16). This period

almost perfectly coincided with the presidency

(1801-1809) of Thomas Jefferson and his policy of “hard

money,” continuous cuts to taxation and expenditure, and

resolute reduction of the national debt.

-

In 1808-1819, PP decreased by 30%

(i.e., from $1.16 to $0.81). During these years, the

U.S. fought the War of 1812 – and incurred much

inflation, taxation and government expenditure, and

added greatly to the national debt. The inflation

culminated in the Crisis of 1819.

-

In 1820-1833, PP increased 88% (i.e.,

from $0.91 to $1.75). During this period, “hard money”

presidents governed; hence taxes and government

expenditures fell. Andrew Jackson, who abolished the

Second Bank of the United States (a forerunner of the

Fed) and repaid all but $38,000 of the national debt,

was most notable in this regard.

-

In 1834-1837, PP fell 22% (i.e., from

$1.69 to $1.32). This period coincided with the

inflationary distortions of state-chartered banks. The

liquidation of these distortions (and many of these

banks) culminated in the Crisis of 1837.

-

In 1838-1861, PP increased 43% (i.e.,

from $1.32 to $1.89). The national debt stood at $15m

when James K. Polk took office in 1845. Fortunately, he

was a hard-money and a low-tariff man; alas, and like

Jefferson and Jackson, he was also a continental

expansionist. He coveted California and Mexico’s other

northern provinces; and to obtain them he resorted to

war. The Mexican War (1846–47) increased America’s

national debt four-fold (to $65m). The next presidents,

Taylor and Tyler, were Whigs; the Whigs were

predecessors of the mercantilist Republican Party; as

such, they were indifferent to government expenditure

and debt. Under their administrations (Taylor died

shortly after taking office), debt ballooned to $80m by

1851. Fortunately, his successor was a Jeffersonian

Democrat – and therefore a staunch practitioner of free

trade, hard money and frugal government. The last of the

Jeffersonians, Franklin Pierce, retired two-thirds of

the national debt, such that it fell to $30m (an amount

less than 5% of GDP) when he left office in 1857.

Neither in absolute amount nor as a percentage of GDP

would the national debt ever again fall so low.

-

In 1862-1865, PP plummeted 41% (i.e.,

from $1.89 to $1.11). These years coincide almost

perfectly with the War to Prevent Southern Independence

(1861-1865), during which the U.S. Government abandoned

the gold standard and undertook a hitherto unprecedented

program of inflation, taxation, expenditure and

borrowing.

-

In 1866-1901, PP increased 83% (i.e.,

from $1.11 to $2.04). During these years, America

returned to the gold standard and Grover Cleveland, its

greatest president since Jackson (and thus staunch

defender of hard money), held office (1885-1889 and

1893-1897). Cleveland doughtily opposed inflation,

imperialism, high tariffs and subsidies to business,

farmers and veterans. He also vetoed legislation more

frequently than any president up to that time. The

Crisis of 1893 occurred between Cleveland’s two terms of

office. In 1902-1913, PP decreased 16% (i.e., from $2.04

to $1.72). During these years, called the “Progressive

Era” in the U.S., the government’s expenditure and

taxation rose, as did its regulation of the economy.

-

In 1914-1920, PP plummeted 51% (i.e.,

from $1.72 to $0.85). In 1913 the Federal Reserve System

commenced operations and in 1917 the U.S. Government

intervened in the First World War. As a result, there

occurred a hitherto unprecedented (that is, bigger than

the Civil War) program of inflation, taxation,

expenditure and borrowing.

-

In 1921-1932, PP increased 55% (i.e.,

from $0.85 to $1.32). The Harding and Coolidge

administrations (we will see that Harding was by far

America’s greatest president of the 20th century)

slashed taxation and expenditure and repaid a

significant portion of the national debt.

-

Since 1933, PP has decreased 94%

(i.e., from $1.32 to $0.08). During these years, in

order to finance the New Deal’s endlessly rising welfare

at home and almost continuous warfare abroad, both the

U.S. Government and Fed have followed a policy of

incessant high inflation (greatly facilitated by the

abandonment of the currency’s link to gold), high and

rising taxation and exponentially growing government

expenditure and borrowing. As a result, in mid-2010

America’s national debt reached $13 trillion (“on

balance sheet”) and up to $100 trillion (“off balance

sheet”) – which means that the U.S. Government is

effectively bankrupt.(4)

America’s bankruptcy is the New Deal’s legacy; as such

(and next only to Abraham Lincoln and Woodrow Wilson) it

makes Franklin Roosevelt the worst president in U.S.

history.

The British figures show remarkably

similar trends. Between 1803 and 1815, Britain fought major

wars in Europe and North America, incurred much inflation,

taxation and government expenditure, and added greatly to

its national debt. As a result, the pound’s PP fell. It

subsequently recovered all of its losses and more: by 1822,

its PP stood 22% higher than it did in 1800. During the next

90 years – which was a time of free trade, the “hard

money” of the classical gold standard, low taxation, small

and balanced budgets and therefore of a government small

enough to fit inside the constitution – the pound’s PP

remained astonishingly stable. As in America and Australia,

so too in Britain: the First World War was a turning point

for the significantly worse. During the War, when the Bank

of England assumed its modern guise as the state’s financier

and manager of the economy rather than a mere custodian of

sound money, the PP of the pound plummeted 62% (i.e., from

£1.39 in 1914 to £0.53 in 1920). As in America and Australia,

so too in Britain: PP then rose by 60% (i.e., to £0.85) in

1936. Finally, in Britain as well as Oz and the U.S., the

Great Depression provided a seemingly permanent turn for the

dramatically worse: since 1936 the pound’s PP’s has

virtually disappeared – to £0.02 (just one fiftieth of its

PP in 1800!) in 2010.

There’s a pattern here, which subsequent chapters will

corroborate. So – ironically – does research conducted under

the Fed’s imprimatur! A study by two economists at the

Federal Reserve Bank of Minneapolis concluded that

“commodity money” standards (namely a classical gold

standard, which subsequent chapters will define and describe)

consistently outperform “fiat” standards. Analysing data

over many decades and from a large number of countries,

Arthur Rolnick and Warren Weber found that “every country in

our sample experienced a higher rate of inflation in the

period during which it was operating under a fiat standard

than in the period during which it was operating under a

commodity [i.e., gold] standard.”(5)

Other members of the establishment are more forthright.

According to Benn Steil and Manuel Hinds of the Council of

Foreign Relations, “the imposition of national [fiat] monies

remains one of the most potent tools available to

governments to extract wealth from their populations and to

exercise political control over them.”(6)

Mainstream economists have long recognised – and some have

overtly celebrated – this brute fact. In The Economic

Consequences of the Peace (Harcourt, Brace & Howe, 1919,

p. 236), for example, John Maynard Keynes gloated

there is no subtler, no surer means of

overturning the existing basis of society than to

debauch the currency. The process engages all the hidden

forces of economic law on the side of destruction, and

does it in a manner which not one man in a million is

able to diagnose.

More specifically, we will see that

welfare and warfare – and the vast amounts of inflation

required to finance them – inevitably weaken and eventually

destroy the currency’s purchasing power. The inflation that

necessarily underpins what we will call the welfare-warfare

state enriches the privileged few; it also foments the

financial crisis on Wall Street that becomes the economic

crisis on Main Street. Conversely, soundly-based money, low

and falling government expenditure, as well as the

reductions of taxation and inflation, augment the currency’s

purchasing power – and also encourage peace at home and

abroad, soundly-based growth and prosperity.

Today, the Australian and American dollars, British pound,

etc., buy vastly fewer goods and services than they once did;

at the same time, wages in these and most other Western

countries have risen – but at a relatively sluggish pace

since the 1970s. The result is that – subject to a

critical caveat – standards of living rose at a rather

robust pace in the three decades after the Second World War,

but at a significantly slower pace since the 1970s. What’s

the caveat? In recent times families have been obliged to

take drastic action to protect their standards of living.

During the 19th century, women (whether single or married)

undertook paid work because economic necessity obliged them

to do so. By the 1950s, however, relatively few married

women worked outside the home. Prosperity had advanced to a

point where a single income often sufficed to provide a

family with a middle class standard of living. That reality

didn’t last long. The campaign waged since the 1970s to

convince women that they are economically equal to men – and

have, therefore, every right to join their husbands in the

workplace, thereby creating a society in which, by the

1980s, most middle-class homes earned two paycheques – has

served as a cover with which to mask the eroding standard of

living over the last 50 years. Today’s middle-class

Americans, Australians, Britons, etc., live much better than

their parents or grandparents did because they enjoy the

benefits of myriad and momentous technological advances

and because both partners must work. Most families could

not service the mortgage, periodically buy a new car and

regularly take holidays, etc., on one income. In the 1950s,

membership of the middle class often required only one

salary; today, it usually requires two.

Why hasn’t this de facto erosion of living standards

angered people? They’ve maintained a material standard of

living that exceeds their forebears’ because technological

advances, a more advanced division of labour and a vastly

heavier load of debt play such important roles in their

lives. They know something that academics and politicians

apparently don’t: the re-entry of women into the paid

workforce is usually not some advanced and noble achievement

of equality; as it was before the 1950s, it’s once again a

brute economic necessity. It’s an essential feature of

modern society because it’s an inevitable consequence of the

central bank’s gradual destruction of the dollar’s

purchasing power. The middle class, in short, has been

fleeced. Many of its members know it, but don’t quite know

how. If a woman wishes to work outside the home, bless her

and more power to her (see in particular Proverbs 31:

11-25), but let’s not pretend that it’s a moral breakthrough.

And let’s reject outright the nonsense that it’s a

consequence of allegedly enlightened attitudes and a benefit

of the modern welfare state. Instead, let’s identify it for

what it is: a consequence of misguided monetary institutions

and poor monetary policies.

In this book we will reason to the conclusion that there’s

only one sensible thing to do with central banks such as the

Reserve Bank of Australia: abolish them and consign them to

the dustbin of history. The mainstream will shriek in horror

at this “radical” conclusion. The real question (which, of

course, they refuse to ask) is: why not rid ourselves

of an institution that has almost completely destroyed the

currency’s purchasing power and has exacerbated the cycle of

boom and bust – particularly when free market arrangements

have shown that money need not lose its purchasing power,

and that they can actually increase it significantly over

long stretches of time?

We’re Radical, But They’re Extremist – and Their Banks

Are Rotten to the Core

“A central bank … must grow like a living organism within

the environment provided by the financial and economic

system in which it exists; its practices and structure must

evolve in response to the needs and demands of that system.”

So wrote H. C. “Nugget” Coombs, the first Governor of the

RBA, in 1951.(7)

I don’t think he appreciated either the significance or the

true meaning of those words. This is because “a central bank,”

as Vera C. Smith wrote in her classic The Rationale of

Central Banking and the Free Banking Alternative (1936),

“is not a natural product of banking development. It is

imposed from outside or comes into being as the result of

Government favours. This factor is responsible for marked

effects on the whole currency and credit structure which

brings it into sharp contrast with what would happen under a

system of free banking from which Government protection was

absent.” In light of Smith’s insight, Coombs unintentionally

affirmed one of this book’s principal findings – namely that

central banks exist not in order to cater the needs of the

general population, but rather to serve (i.e., finance) the

state that creates them. As a result, and as we shall see, a

small number of “insiders” gains handsomely and the mass of

“outsiders” loses heavily.

We will also demonstrate from first principles and in simple

language that

-

For centuries, fractional reserve

banks – which we’ll define and describe in detail, and

which comprise virtually all contemporary banks – have

misappropriated depositors’ funds and counterfeited

money. Contemporary monetary institutions, practices and

policies, in other words, are built upon a foundation of

“legalised” fraud.

-

For this reason, and also as a

consequence of their inherent illiquidity, fractional

reserve banks are at all times, and not just during

financial and economic crises, bankrupt. Without the

constant and active intervention of the state in general

and its central bank in particular, their bankruptcy

would be plain for all to see.

-

Central banks don’t fight

inflation: they manufacture and maintain it.

These days, only the actions of commercial and central

banks can create inflation. The legislation and

regulations that underlie the banking system inflate the

boom that inevitably busts.

-

The state has embedded its protections

of commercial banks so deeply within legislation and

regulations – in other words, it has extended such

enormous privileges to banks for such a long time – that

virtually nobody now recognises bankers for what they

have always been: massively featherbedded white-collar

wharfies.

-

When examined in the light of

Christian theology (particularly of St Augustine of

Hippo, St Thomas Aquinas, Bishop Nicolas Oresme and

Popes Pius XI and John Paul II), central and fractional

reserve banking is certainly deeply immoral and likely

anti-Christian.

This book’s premises and conclusions are

radical in the proper sense of the term – they dig to

the roots and sources of the monetary sickness that pervades

Western societies. We will start from first principles and

justify our logic and evidence every step of the way. But

our approach and results are emphatically not extremist:

by highlighting current arrangements’ pervasive violations

of traditional legal principles and rights to private

property, we will see that today’s defenders of the

status quo are the real extremists. (...)

|